Author: Roberto Rios (@peruvian_bull)

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Jane Street is the most profitable quantitative trading company in Wall Street history, yet few know of its existence—until this week when it was accused of insider trading leading to the Terra Luna crash, while also embroiled in a $560 million index manipulation lawsuit in India. This article connects Jane Street's alleged manipulation of Terra Luna, market manipulation in India, and the daily 10 a.m. Bitcoin dump known as the "10 AM Smash" into a complete investigative chain, with timelines and data that withstand scrutiny. Bitcoin's rebound today may be tied to this story.

Full Text Below:

The most powerful trading company you've never heard of was just caught with its hand in the cookie jar. Twice. On two different continents.

And Bitcoin, finally, is set free because of it.

Follow me:

Jane Street Group is a New York-based quantitative trading firm. They have no CEO.

By their own description, the company operates like an "anarchist commune." In just the first nine months of 2025, they recorded net trading revenue of $24 billion, surpassing the $20.5 billion for all of 2024. In Q2 2025 alone, they achieved $10.1 billion—the highest quarterly trading revenue ever recorded by any company in Wall Street history.

By any measure, Jane Street is the most profitable trading institution on Earth.

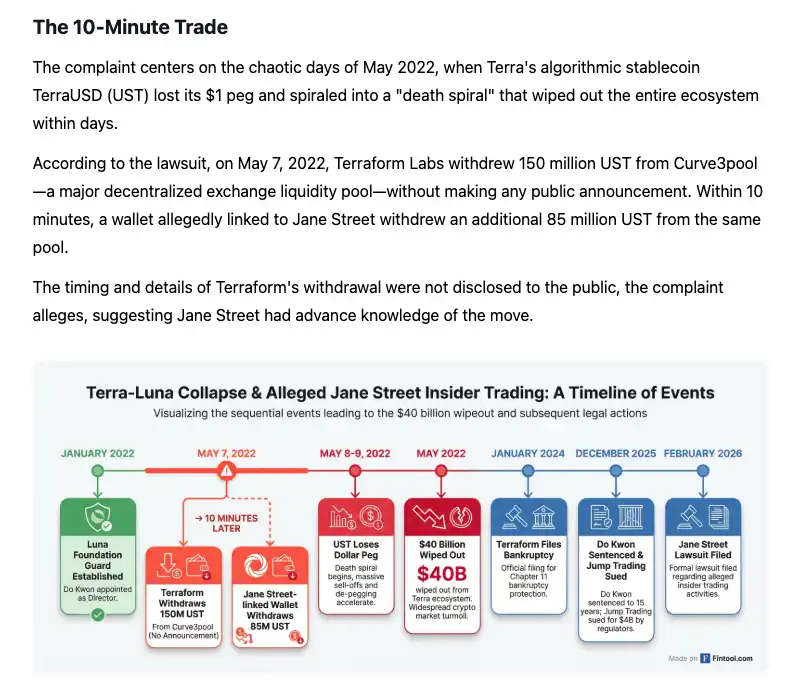

And just this week, the Terraform Labs bankruptcy administrator filed a lawsuit in Manhattan federal court, accusing Jane Street of using insider information to position itself ahead of and profit from the May 2022 collapse of Terra Luna. That crash wiped out $40 billion in value and triggered a chain reaction that ultimately brought down Celsius, Three Arrows Capital, and FTX.

The logic of the accusation is stunningly simple.

On May 7, 2022, Terraform Labs quietly withdrew $150 million in UST from the Curve 3pool, a major decentralized liquidity pool. No announcement, just a silent liquidity withdrawal.

Ten minutes later, a wallet linked to Jane Street withdrew $85 million from the same liquidity pool.

A full ten minutes.

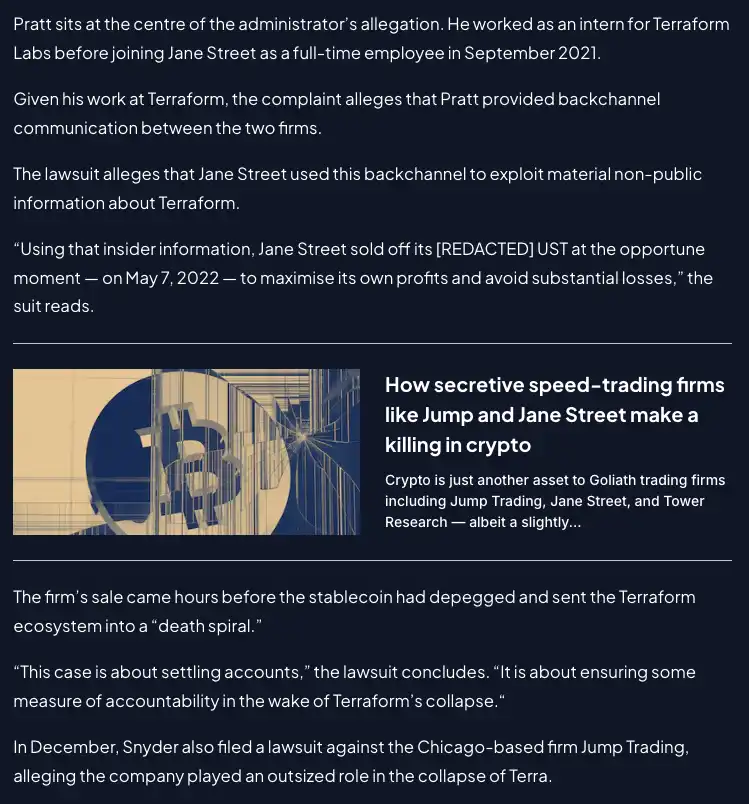

The lawsuit alleges that a former intern at Terraform, Bryce Pratt, who joined Jane Street as a full-time employee in September 2021, established a secret communication channel with his former colleagues at Terraform. He is accused of directly conveying material non-public information about Terraform's liquidity operations to Jane Street's trading desk.

The lawsuit names four defendants: Jane Street Group LLC, co-founder Robert Granieri, and employees Bryce Pratt and Michael Huang.

The bankruptcy administrator's statement cuts to the chase: The trades executed by Jane Street "would not have been possible without access to material non-public information to which they were exclusively privy."

It gets worse. The lawsuit alleges that Jane Street's withdrawal helped trigger the de-pegging of UST, pushing the entire Terraform ecosystem into a death spiral. LUNA fell from over $80 to near zero. $40 billion evaporated. Ordinary people lost everything—retirement savings, education funds, a lifetime of accumulation, gone in days.

Jane Street's response? They call it a "desperate move by those with their backs against the wall," "baseless allegations."

But the problem is, this isn't their first time.

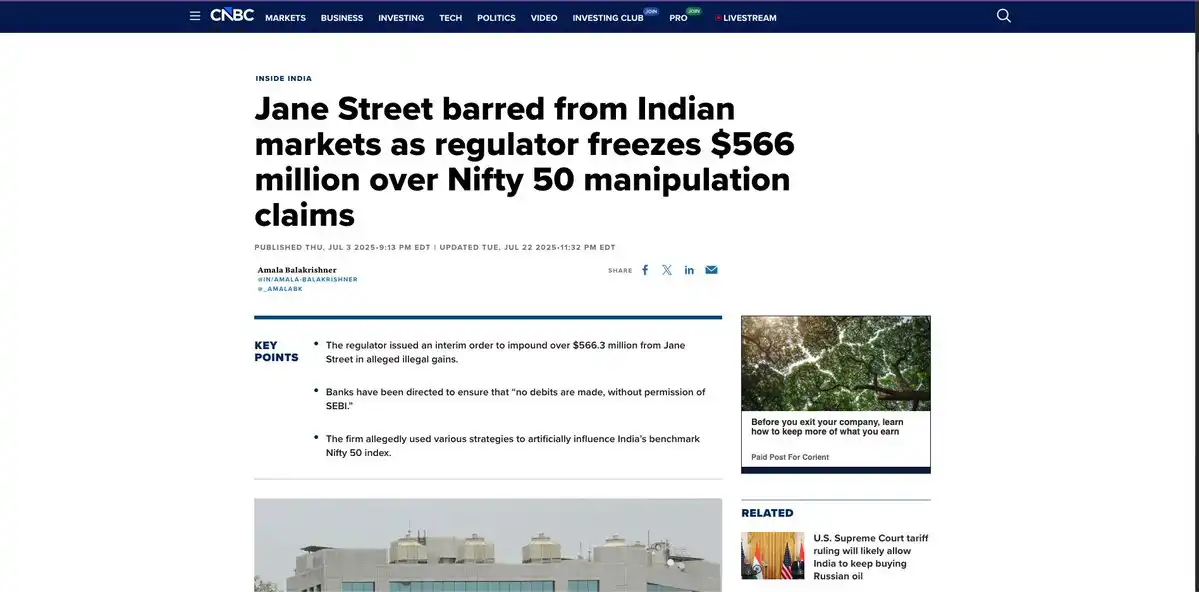

In July 2025, the Securities and Exchange Board of India (SEBI) brought one of the largest market manipulation charges in Indian history against Jane Street. SEBI's investigation found that on 18 derivative expiry days between January 2023 and March 2025, Jane Street executed a textbook pump-and-dump manipulation of the Bank Nifty index.

The operation was mechanically precise:

Morning: Jane Street's algorithms heavily bought Bank Nifty component stocks and futures, pushing the index up 1% to 1.3%. SEBI found that on some trading days, Jane Street alone contributed to the entire positive price impact of the index.

Simultaneously, they built large short option positions, primarily selling calls and buying puts, with the size of their options positions severely disproportionate to their stock holdings. SEBI found that, in delta equivalent terms, their options positions were 7.3 times larger than their stock and futures positions. This wasn't hedging, this wasn't arbitrage; this was directional manipulation with extra steps.

Afternoon: They reversed and sold all the stocks bought in the morning, the index fell, the short options profited, rinse and repeat, every expiry day.

SEBI's ruling: Illegal profits of 4.843 billion rupees, approximately $580 million. They characterized Jane Street's actions as a "deliberately designed means to manipulate the settlement price." SEBI also specifically noted that Jane Street continued this strategy even after the National Stock Exchange of India issued a clear warning in February 2025.

SEBI's wording was unusually harsh, rare for a regulator: "The integrity of the market, and the trust of millions of small investors and traders, can no longer be held hostage to the machinations of such an untrustworthy participant."

Jane Street was banned from the Indian securities market. They deposited over $560 million into an escrow account and immediately appealed. As of today, the case is still under review at the Securities Appellate Tribunal in India.

Now, about Bitcoin.

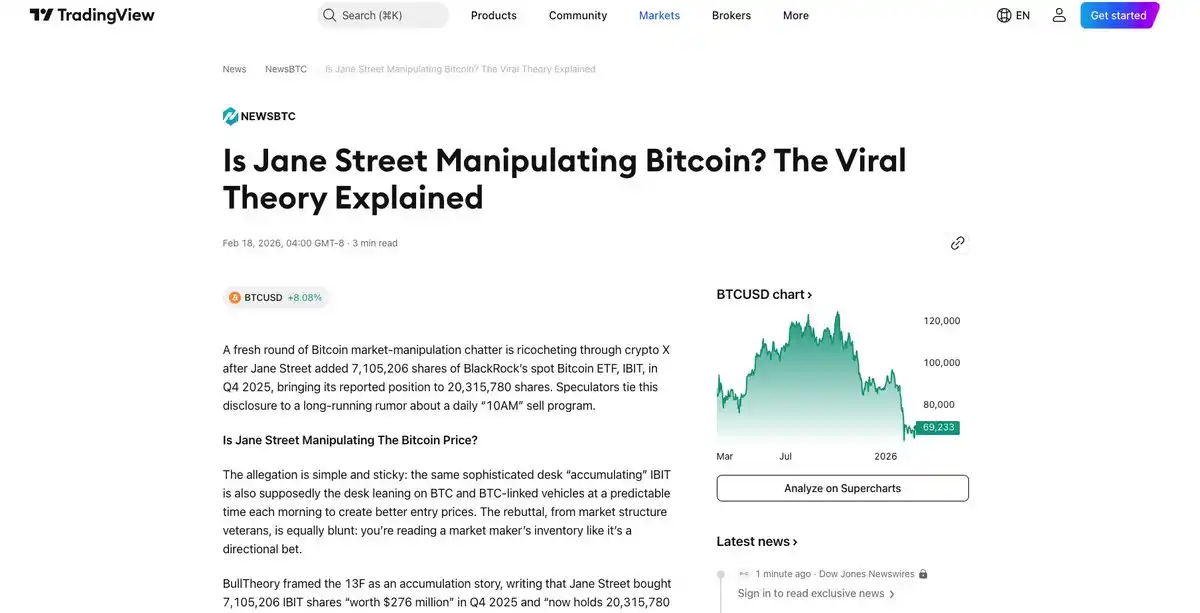

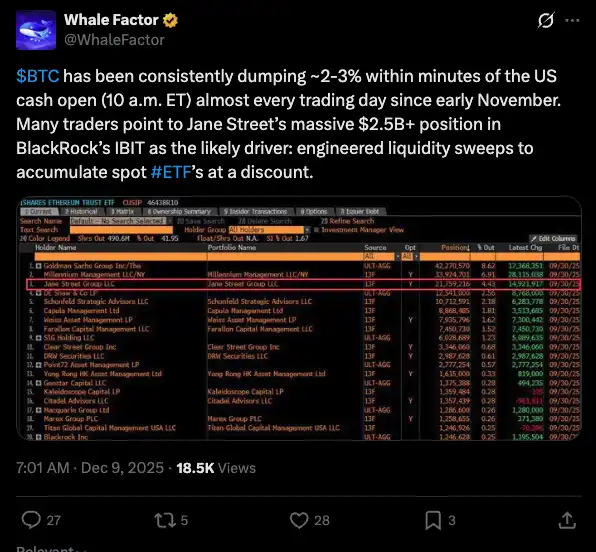

Since November 2025, Bitcoin traders noticed a strange pattern: every morning around 10 a.m. ET—coinciding with the US stock market open—heavy selling would hit BTC and related ETF shares.

This pattern was eerily consistent. Bitcoin would rise during Asian and European trading hours, only to be suppressed as soon as New York opened.

(See: https://www.tradingview.com/news/newsbtc:f65a83ede094b:0-is-jane-street-manipulating-bitcoin-the-viral-theory-explained/)

The numbers were staggering. Charts from December 2025 showed BTC falling from $89,700 to $87,700 in minutes on some days, liquidating $171 million in leveraged long positions before the price recovered. This occurred on December 1st, 5th, 8th, 10th, 12th, 15th, and repeated throughout January and February 2026.

Crypto Twitter dubbed it the "10 AM Smash."

Fingers pointed squarely at Jane Street, for good reason. Jane Street is one of only four Authorized Participants for BlackRock's IBIT, the world's largest spot Bitcoin ETF. The other three are Virtu Americas, J.P. Morgan Securities, and Marex. As an Authorized Participant, Jane Street has the unique ability to create and redeem ETF shares, meaning they have direct access to the pipeline for Bitcoin moving in and out of the institutional wrapper.

Their 13F filings confirm massive holdings. Jane Street held $5.7 billion worth of IBIT shares as of Q3 2025. In Q4, they added another $276 million, bringing their total holdings to over 20 million shares, worth approximately $790 million at year-end prices. At their peak, they held nearly $2.5 billion in IBIT.

But one thing was suspicious: While allegedly selling spot BTC every morning, Jane Street increased its MSTR (Strategy, formerly MicroStrategy) position by 473% in Q4 2025, buying 951,187 shares worth approximately $121 million. This happened while major funds like BlackRock and Vanguard were selling billions of dollars worth of MSTR.

Think about what this implies: Sell BTC at the open, push the price down, liquidate leveraged longs, buy back lower. Meanwhile, heavily buy the most leveraged Bitcoin proxy on the market, waiting for the inevitable price recovery.

Glassnode co-founders Jan Happel and Yann Allemann, through their Negentropic account on X, reignited this theory, linking the algorithmic trading patterns to the filing of the Terraform lawsuit. The Milk Road account amplified the message further, describing "persistent whispers" about institutional trading desks executing a "very specific and conspiratorial playbook."

Then, the lawsuit came. Then, something unexpected happened.

After the Terraform lawsuit against Jane Street was filed, the "10 AM Smash"... didn't happen. For the first time in months, Bitcoin wasn't suppressed at the US market open; instead, it rose.

Today, February 25, 2026, Bitcoin surged over 3%, breaking through multiple resistance levels, trading above $68,000, just days after threatening to fall below $60,000. $323 million in short positions were liquidated. The Stochastic RSI hit 100. ETFs saw a net inflow of $257.7 million for the day, the highest since early February.

https://x.com/peruvian_bull/status/2026730420168192432?s=20

The pattern broke.

I want to be careful here. Correlation does not equal causation. Multiple factors were at play simultaneously: Trump's State of the Union, oversold technicals, short covering. The Fear & Greed Index was at 11, extreme fear, which is often a contrarian turning point. The RSI had fallen to 15.80, a reading not seen since the COVID crash of 2020, which was followed by a 1400% rally. But the timing coincidence is hard to ignore.

Rumors circulated on X that Jane Street was "forced to shut down its trading algorithms" after the lawsuit was filed. Jane Street told Cointelegraph these were "baseless speculative allegations." Whether they were forced to stop or paused out of legal prudence, the result was the same:

The selling pressure vanished.

What this really means for Bitcoin.

Bitcoin spot ETFs were supposed to be the great equalizer. Institutional access, regulated products, BlackRock's stamp of approval. And they have been wildly successful—IBIT alone has attracted over $20 billion in inflows since launch.

But the ETF structure introduced something Bitcoin was specifically designed to escape: trusted intermediaries with privileged access to the pipeline.

When the SEC approved Bitcoin spot ETFs in January 2024, it required cash-only creation and redemption. Whenever shares needed to be created or redeemed, someone had to actually buy or sell Bitcoin. And the firms with access to this process—the Authorized Participants—held a structural advantage over every other market participant.

In September 2025, the SEC approved in-kind creation and redemption for IBIT, meaning Authorized Participants could now exchange Bitcoin directly for ETF shares, bypassing the fiat step. This gave Jane Street, Virtu, J.P. Morgan, and Marex more direct control over the flow of Bitcoin in and out of the largest institutional wrapper.

The "10 AM Smash" is essentially a symptom of the same disease that has plagued the gold market for decades.

I wrote about this in "The Final Gold Game Begins": Paper trading against paper trading, where the institutions with the most access to the pipeline can move the price before the rest of the market can react.

https://x.com/peruvian_bull/status/1778146092279861279?s=20

J.P. Morgan traders Gregg Smith and Michael Nowak were convicted of placing fraudulent orders in the precious metals futures market, a scheme that lasted eight years and involved thousands of illegal trades. J.P. Morgan paid a $920 million settlement. Deutsche Bank paid $30 million for the same behavior. UBS, HSBC, and six individual traders all faced CFTC charges for anti-fraud violations.

Same playbook, different asset.

Every time, these firms call it "market making," "arbitrage," "hedging." The euphemisms are endless, the result always the same: The little guy gets carved up, and the insiders capture the spread.

So, where do we go from here?

The broader structural picture hasn't changed. $4.5 billion in ETF net outflows in the first eight weeks of 2026 looks concerning, but Strategy (Saylor's company) just bought $39 million worth of BTC, accounting for 99% of all public company purchases in that period. The big players aren't selling; they were waiting for the algorithms to do their work.

And perhaps, just now, the algorithms are finished.

If Jane Street—whether due to legal exposure, regulatory scrutiny on multiple continents, or simple self-preservation—has been forced to retreat from its alleged daily selling program, it means a persistent structural resistance that has suppressed Bitcoin for four months has been removed.

Bitcoin was born for this moment. A monetary system that doesn't rely on trusted intermediaries, doesn't need Authorized Participants, and cannot be front-run by messages from a former intern passed through a secret pipeline to a trading desk.

But don't forget how we got here. The very firms that were supposed to "make markets" and "provide liquidity" are the same ones accused of front-running a collapse, manipulating a national stock index, and running an algorithmic selling program daily against the very asset their ETF was supposed to track.

This is the very system Bitcoin was designed to replace.